What Entrepreneurs Need to Know About Incorporating Franchises

According to Statista, there were an estimated 732,842 franchise establishments in the United States in 2016 and 2017 is poised to see an uptick in that number to 744,437. As franchise establishments become more popular with entrepreneurs, they might wonder if there are any extra incorporation notes they need to keep in mind. There are subtle differences that small business owners need to be aware of during the entity formation process. We’ve outlined what to keep in mind when incorporating an existing franchise or a business that will eventually become a franchise below.

Incorporating an existing franchise

Imagine that you want to buy and own a Subway franchise. There are plenty of advantages in doing this—right away, you’ll get training, support, and brand name recognition that can provide your business with a credibility boost to translate to sales. But there are also obligations tied to becoming a franchise owner. The Federal Trade Commission states that franchisors need to pay costs, like initial franchise fees, be aware of franchisor controls on everything from site approval to appearance standards, and comply with contractual obligations in exchange for the right to use the franchisor’s name and benefit from it. Oh, and run the business too!

If you’ve decided that you’re ready to invest, picked the right franchise for your abilities and consumer demands, reviewed the Franchise Disclosure Document (FDD), and signed the Franchise Agreement, you’ll want to figure out which legal structure is the best choice to protect the franchise.

If you decide to form an LLC, then you’ll be able to keep your personal assets separate from the franchise. You’ll also be subjected to favorable tax treatment, since LLCs are treated as a “pass-through” entity with single taxation. As a legal structure, a Corporation offers the same liability protection for personal assets that LLCs provide. Corporations are more formally structured than LLCs, which is good news for entrepreneurs that want to own even more franchises as this entity reduces potential audit risk.

Turning your business into a franchise

This one is a little different from buying an existing establishment since you’re starting with a small business and grooming it for franchise success. If your business offers products or services that stand out from the crowd but still bring in customers because they’re so in demand, then it’s worth looking into spinning this idea off into a franchise.

As far as incorporating goes, we circle back to the benefits of LLCs and Corporations. LLCs offer liability protection and the flexibility to run the business with a few members. For your tax entity, you have the option to choose between an S-Corporation and C-Corporation. For Corporations, the formal business structure is attractive to potential investors to invest capital in, should you decide to grow the franchise on the same level as Subway.

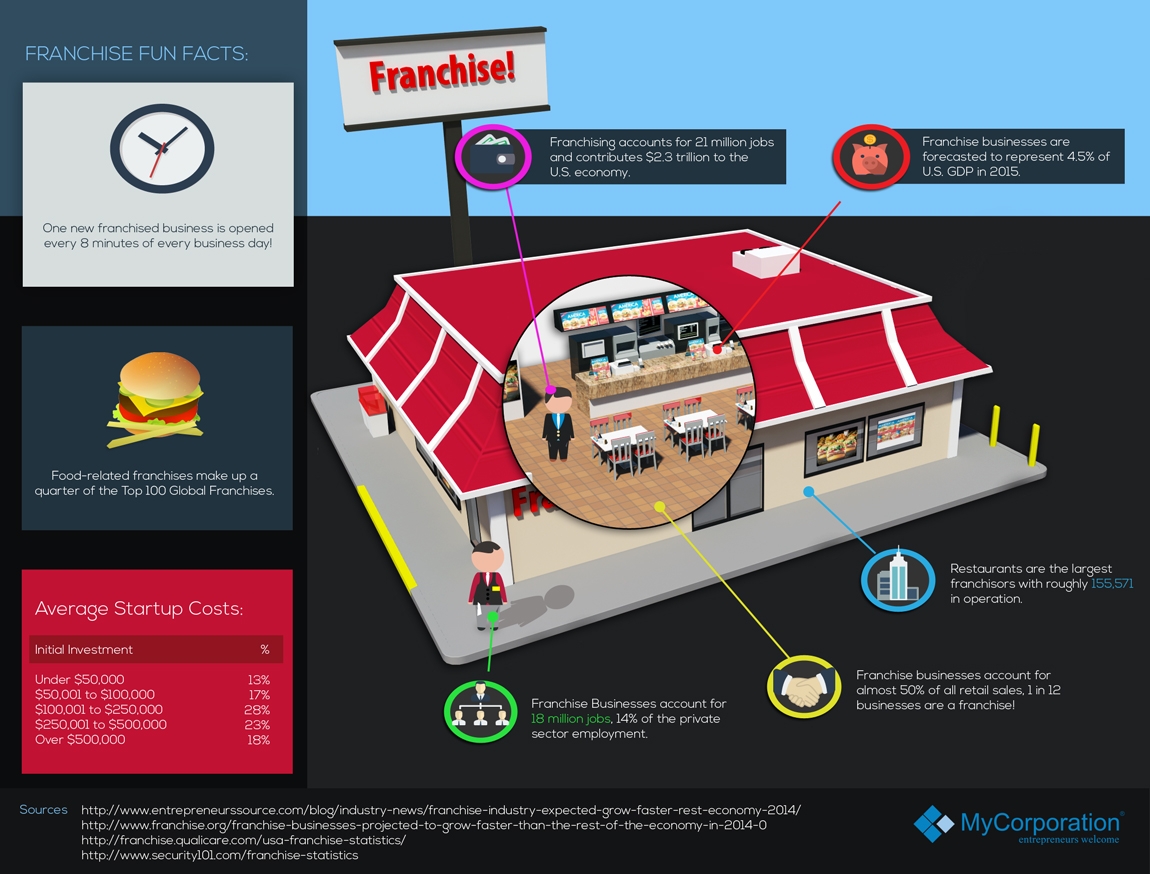

However, turning your business into a franchise is still an expensive, and risky, endeavor. Your offering must be a concept that’s easy to teach and duplicate and should be in demand with customers. Entrepreneurs should also be willing to research everything about the competition that they can, put in hard work, and be able to navigate potential regulatory obstacles. If your idea is unique and worthy of becoming a franchise, then legitimize the business and go for it! After all, every eight minutes of every business day, a new franchised business is opened — and the next one could be yours.

{kind=link}